Every day, usually sometime between 5 and 7 p.m.—or, apparently, any hour in Monterrey—almost every city in the world experiences the same frustrating traffic.

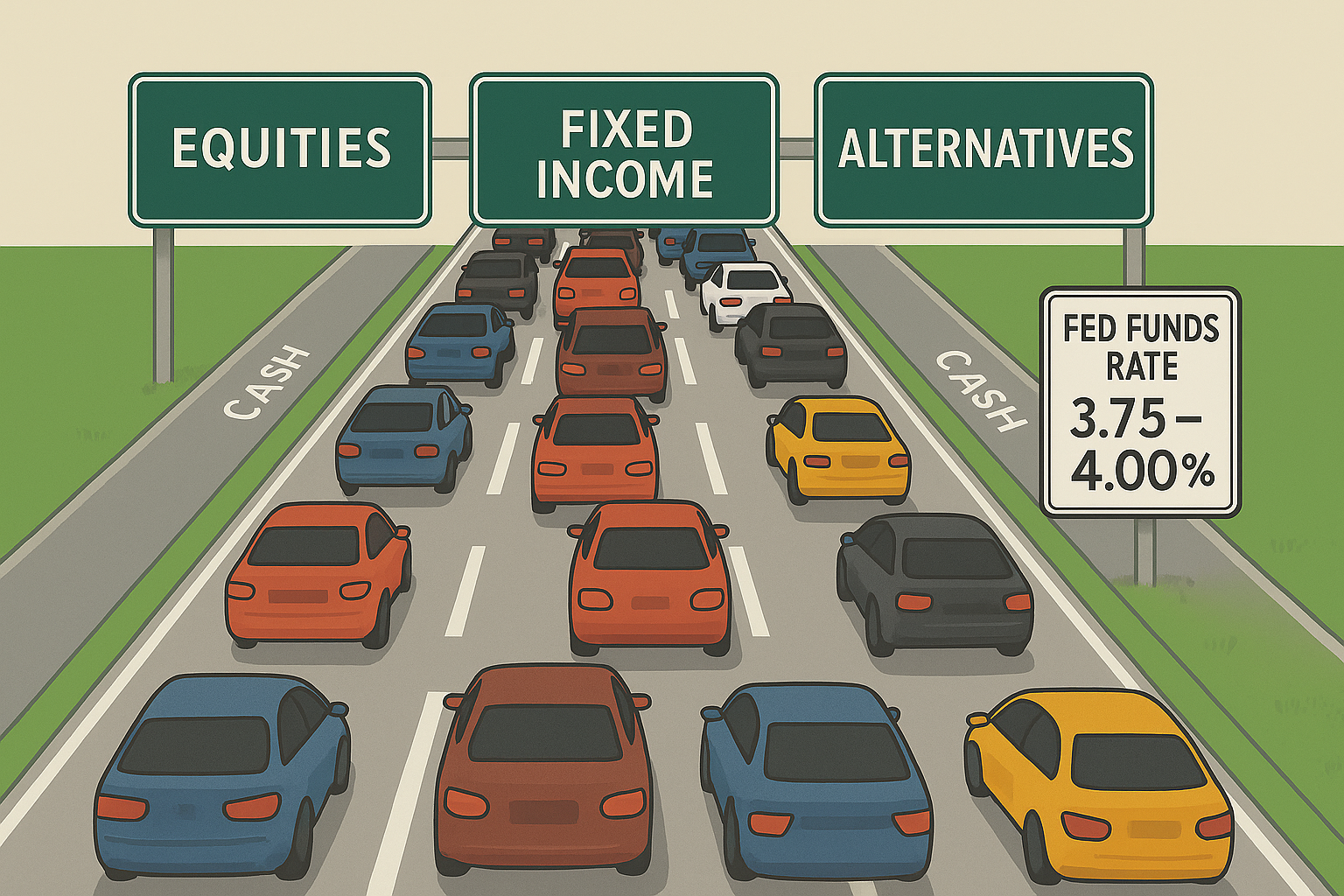

Three lanes of cars suddenly frozen in place. The left lane, which is supposed to move faster, is full of impatient drivers. The middle lane moves slowly but steadily. The right lane, meant for exits, sits mostly empty—until clever or desperate drivers use it to skip the line.

This small moment of urban chaos can actually say a lot about how the financial world works. On closer inspection, those three lanes mirror the three main asset classes in modern markets. The left lane represents equities, the middle fixed income, and the right alternatives. Each lane attracts a different kind of investor, operating at a different speed and bearing a different level of risk.

The Fast Lane: When Consensus Becomes Congestion

The stock market often resembles the fast lane on a highway. When traffic is flowing, that is where everyone wants to be—it feels like progress, momentum, and control all at once. Stocks move quickly. They reward courage and give investors the comforting illusion that they are steering their own direction. When the economy expands and optimism builds, money naturally drifts left, chasing the thrill of acceleration.

Anyone who has spent enough time on the road, however, knows what happens when too many switch to the same lane: congestion.

The same reflexive pattern plays out in markets. During bubbles—from the tech mania of the late 1990s to the meme-stock rush of 2021—investors crowd into the same trades, convinced they will be the ones to outperform and that it is not too late.

Economist Hyman Minsky warned of this cycle in "Stabilizing an Unstable Economy": long stretches of calm make people forget risk, encouraging leverage and speculation until the system becomes fragile.

Then one small brake check—an earnings miss, a rate hike, a shift in sentiment—ripples through the flow. Panic spreads, and the market, like traffic, comes to a standstill.

The left lane rewards confidence, but it never forgives recklessness. When too many people switch at once, the whole system freezes.

This is what economists mean when they say markets are "reflexive"—our actions change the system itself. When all investors or drivers are merging or unsure, returns can become constrained.

What George Soros described as reflexivity—the two-way interaction between market participants’ thinking and the situation they participate in—functions like a feedback loop: belief affects behavior, and behavior changes reality.

The Middle Lane: Where Safety Becomes Complacency

The bond market is a lot like the middle lane on a highway. It is where the big, steady players like pension funds, governments, and cautious investors prefer to drive. Bonds do not offer much excitement, but they promise predictability. They are meant to be the "safe" option, the lane where you can relax your grip on the wheel.

That said, “safe” does not mean risk-free. When central banks raise interest rates, bond prices fall. That is exactly what happened around the world in 2022 and 2023, when inflation forced policymakers to tighten monetary policy. Investors who treated bonds as untouchable suddenly faced their steepest losses in decades.

The bond selloff of 2022 was the equivalent of a stalled vehicle in the middle lane—a sudden obstruction that shattered the illusion of steady, unimpeded progress.

As economist John Maynard Keynes observed in The General Theory, worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally—or as the idea is often paraphrased, most investors would rather be conventionally wrong than unconventionally right.

The middle lane feels comfortable precisely because everyone else is there.

When you are bumper-to-bumper in the middle lane, you do not blame yourself for the jam; you assume everyone else is stuck too, that it could not have been avoided.

Bond investors think the same way. When the economy slows or inflation arrives unexpectedly, they see it not as a mistake of judgment but as an inevitable consequence of the road itself. In both cases, the feeling of safety comes not from control, but from shared inconvenience.

The Exit Lane: Where Innovation Meets Volatility

Finally, we have the right lane—the one meant for exits, but most often used by drivers who think they have found a faster way through. In finance, this lane represents the world of alternative investments and entrepreneurship: venture capital, private equity, and more recently, crypto.

It attracts those who have grown restless with the slow pace of traditional finance and want to build or bet on something new, much like drivers annoyed at the pace of traffic in the other lanes.

Entrepreneurs and early-stage investors operate here because it offers freedom of movement. They accept volatility in exchange for autonomy. While this lane can be uneven, it is also where wealth creation compounds fastest when conviction meets timing—provided the road is clear of obstacles.

The Metaphor Extends

The point, however, is clear.

It is not about picking the right lane forever—it is about understanding the flow. Equities reward risk, Fixed Income rewards patience, and Alternatives reward imagination, but none of them guarantee safety. What matters is judgment: knowing when to accelerate, when to yield, and most importantly, when to leave.

Rewards confidence

Punishes recklessness

Watch for: congestion

Rewards patience

Punishes complacency

Watch for: rate shifts

Rewards imagination

Punishes poor timing

Watch for: potholes

- Minsky, Hyman P. Stabilizing an Unstable Economy. Yale University Press, 1986.

- Soros, George. The Alchemy of Finance. Simon & Schuster, 1987.

- Keynes, John Maynard. The General Theory of Employment, Interest and Money. Macmillan, 1936. Chapter 12.

- Shiller, Robert J. Irrational Exuberance. Princeton University Press, 3rd ed., 2015.

- J.P. Morgan Asset Management. Guide to the Markets. Q4 2025.

- Bloomberg. U.S. Aggregate Bond Index, total return data 2020–2024.

- Cambridge Associates. U.S. Venture Capital Index, quarterly benchmarks.

- Morningstar Direct. Meme stock YTD return data, December 2021.